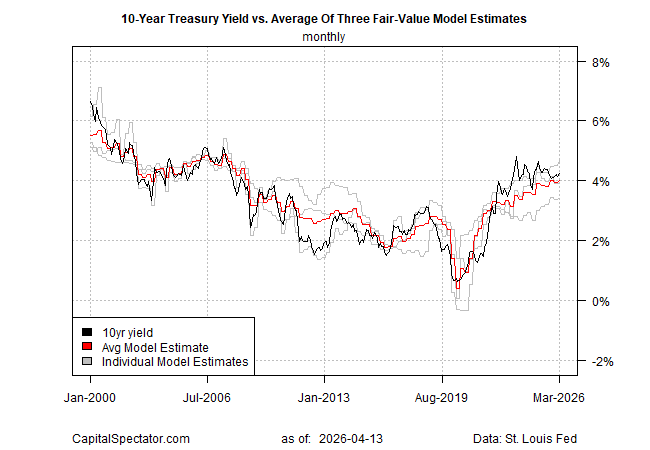

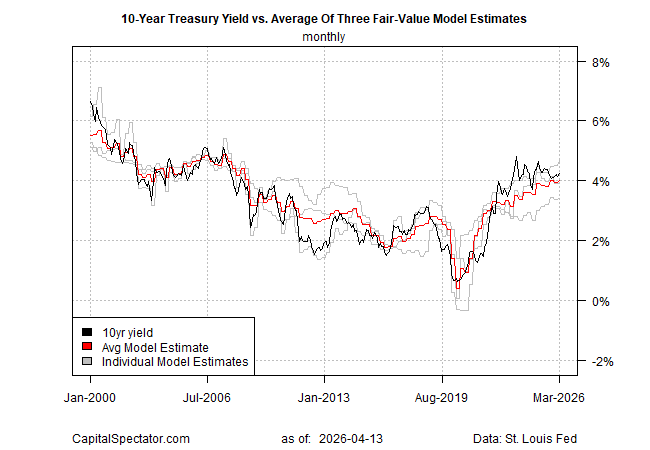

How much policy uncertainty and geopolitical risk can the US economy absorb without derailing its expansion? More than many analysts expected.

As a thought experiment, let’s return to Jan. 1, 2025. Your task is to consider what the economic impact would be if the global trading system were upended with tariffs and a major war in the Middle East sharply raised energy costs. Would those events disrupt the US economy, perhaps to the point of triggering recession? Answering “yes” would have been a reasonable forecast. But here we are, and economic activity—although battered and bruised by some measures—is still skewed toward growth overall.

How long this lasts is unclear, but a review of several indicators suggests that US economic resilience has been more durable than many of us would have expected when gaming out a world of tariffs and war with Iran.

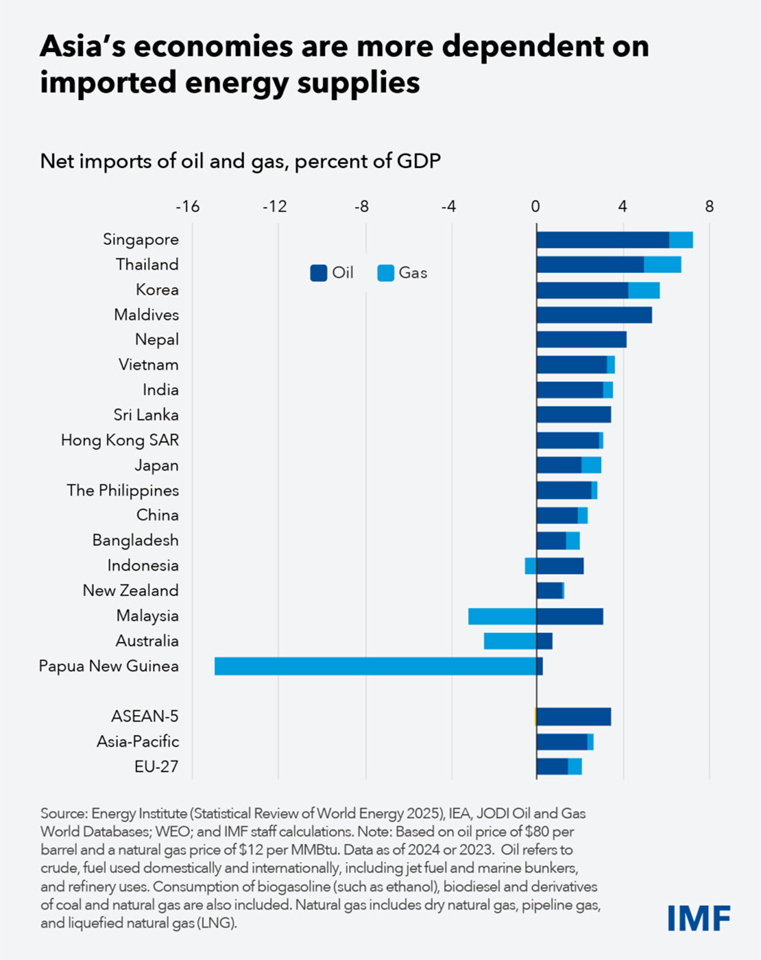

Part of the reason is US energy independence. As a net energy exporter, the economy’s reliance on oil imports is low. That doesn’t shield the country from surging energy costs — oil is priced globally, not locally. But compared with the high dependence on imported oil in Asia, for instance, the US is in far better shape to weather a supply-side energy shock.

There are limits to US resilience, of course, and those limits may be near. Much depends on how long oil prices (and energy costs generally) remain elevated. As I discussed yesterday at TMC Research, the risks of higher inflation and slower growth will rise the larger the potential shock to the economy in the months ahead.

“After withstanding higher trade barriers and elevated uncertainty last year, global activity now faces a major test from the outbreak of war in the Middle East,” the IMF warned yesterday. “A longer or broader conflict, worsening geopolitical fragmentation, a reassessment of expectations surrounding artificial intelligence–driven productivity, or renewed trade tensions could significantly weaken growth and destabilize financial markets.”

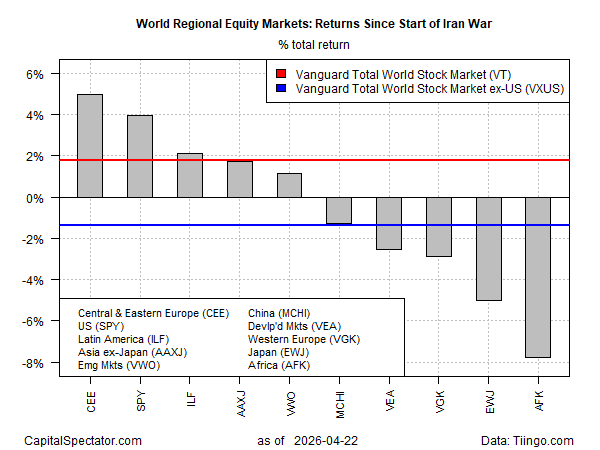

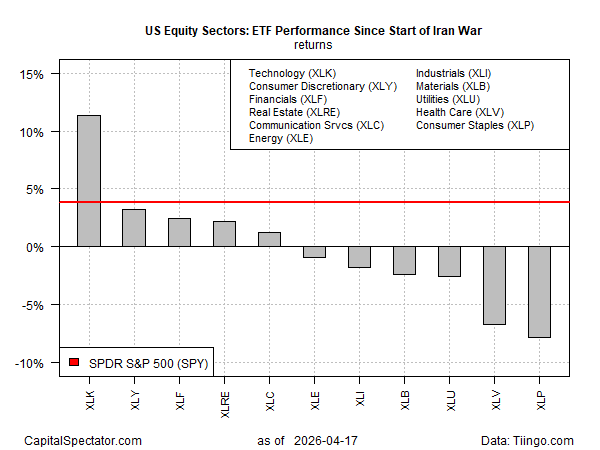

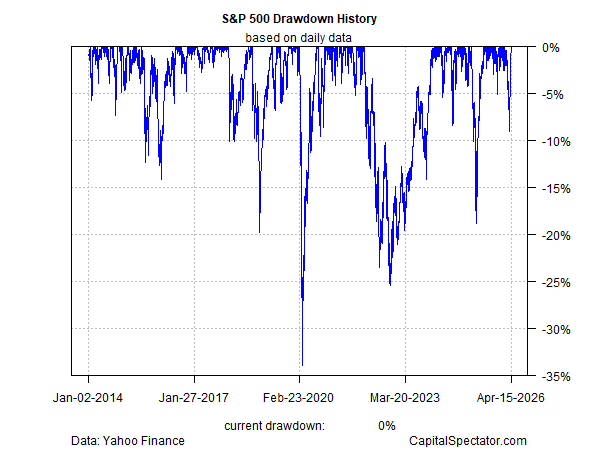

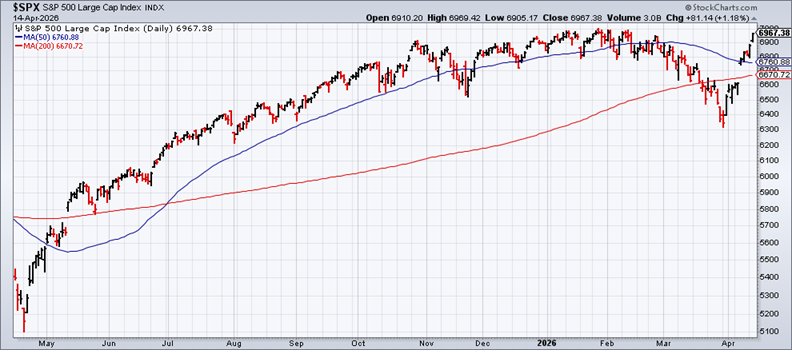

The US stock market, however, appears to be pricing in higher odds that the worst has passed. The S&P 500 Index yesterday (Apr. 14) rallied for a second day, recovering nearly all of the loss since peaking earlier in the year.

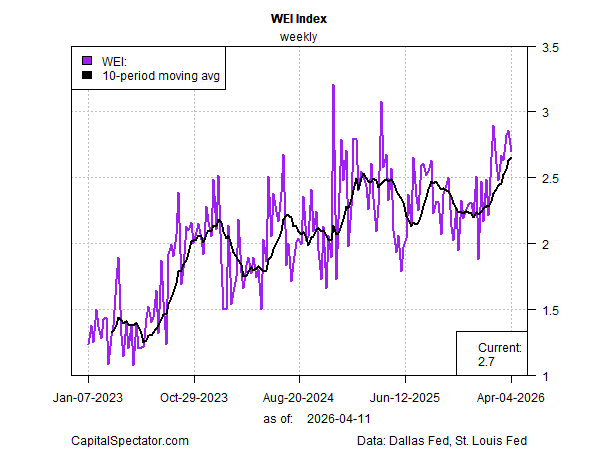

The stock market isn’t the economy, as the caveat goes, but several proxies for the business cycle suggest a growth bias is holding. For example, the Dallas Fed’s Weekly Economic Index (WEI) reflects real year-over-year economic growth of 2.7% through Apr. 4. That’s up from a 2.0% pace through last year’s fourth quarter, based on GDP data.

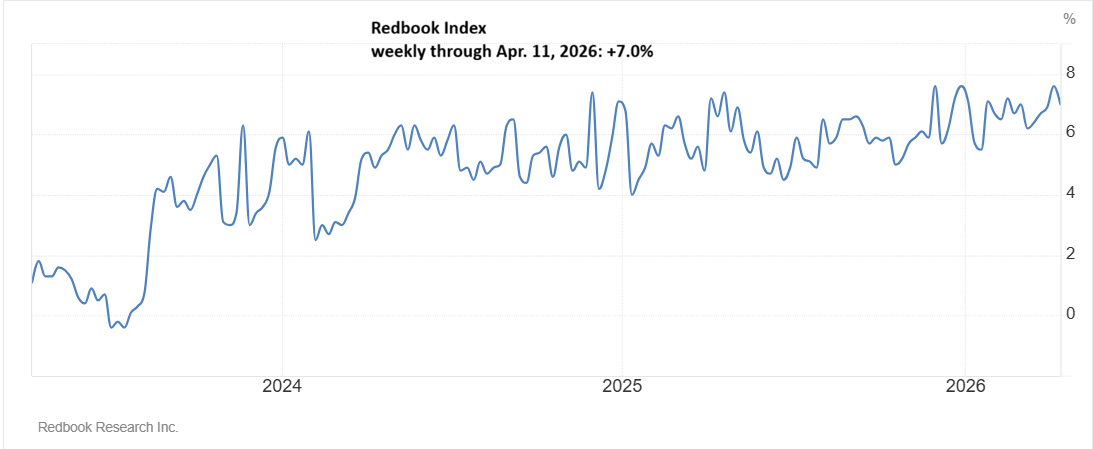

Several other real-time measures of economic activity also point to ongoing resilience. The Johnson Redbook Index—a weekly year-over-year measure of same-store sales growth for large US general merchandise retailers (roughly 80% of retail sales)—rose 7% for the week through Apr. 11, in line with the trend in recent months. The implication: consumer spending has yet to take a hit from the war.

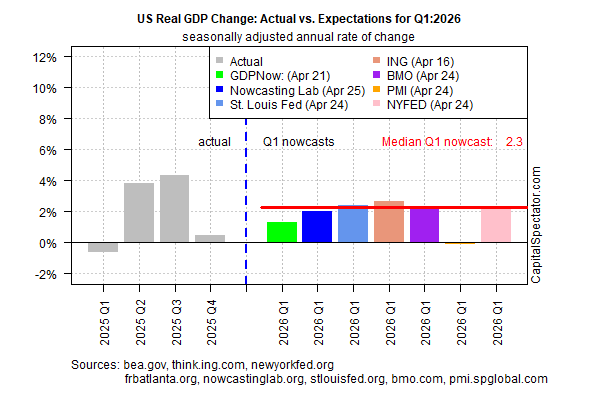

None of this is to suggest that there are no warning flags. Au contraire. The sharp rise in headline consumer inflation in March suggests that the war’s effects on the economy and spending may not be trivial. Add to that the possibility that economic growth could be sluggish in the upcoming Q1 GDP report, according to the Atlanta Fed.

One measure of consumer sentiment is also flashing red. “Consumer sentiment sank about 11% [in April], extending a decline that began with the start of the Iran conflict, and is currently about 9% below a year ago,” according to the University of Michigan’s widely followed survey.

In the hard data, by comparison, the signs of trouble for the US economy are still limited. It would be naïve to expect no repercussions. But the blowback so far has been minimal, at least from a top-down perspective. But economic data arrives with a lag and so the brunt of the war’s effects will likely become clearer in the weeks and months ahead.

Watching the incoming data, in short, is a high priority. Meanwhile, the US economy appears to be beating the odds by staying resilient. The relative strength has surprised more than a few keen observers of the economic scene.

“It is notable that client sentiment, especially in the US, seems quite resilient considering the amount of uncertainty you have in the Middle East,” says Jeremy Barnum, JPMorgan’s chief financial officer.

A fragile peace in the war with Iran continues, which lays the groundwork for cautious optimism. A resumption of hostilities, by contrast, would likely be cause for downgrading resiliency expectations. By that standard, evaluating macro risk remains a day-to-day affair.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}