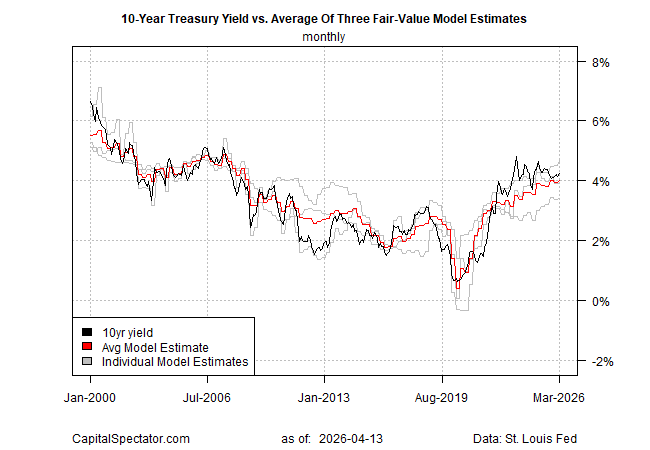

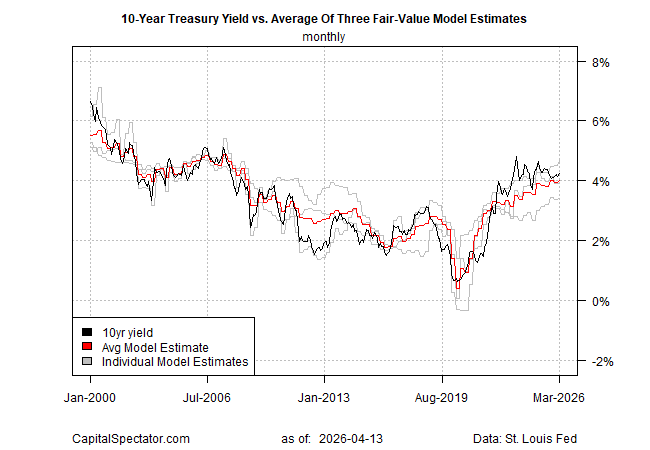

Stock Market At Record High as Iran Crisis Deepens

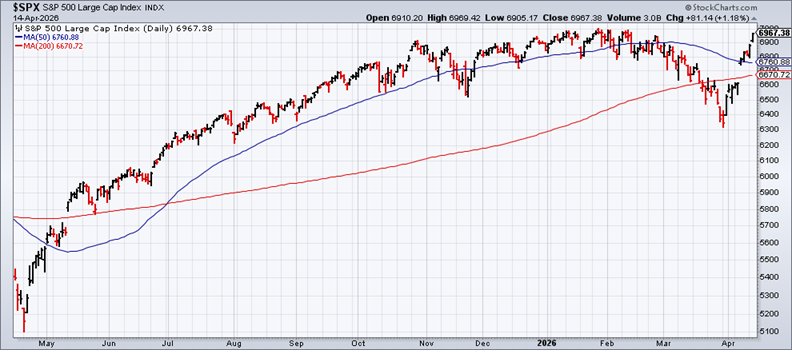

The US stock market closed at a record high on Friday (Apr. 17), but a few days ago is ancient history when the firehose of war news can reshape investor sentiment by the hour. Right on cue, the trading week ahead has plenty of fresh shape-shifting headlines to process and decide if last week’s optimism revival still resonates.

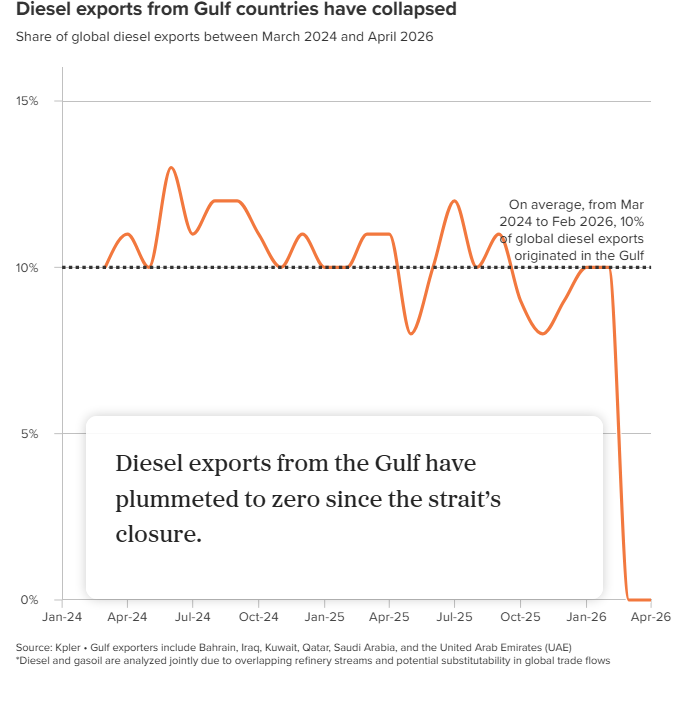

Among the highlights over the weekend: Iran reversed its earlier agreement to reopen the Strait of Hormuz to restart energy exports, with hardliners in the country asserting control and insisting it will remain shut as long as the US blockade continues. A US Navy ship fired on an Iranian cargo ship violating America’s blockade, later seizing the vessel. Iran vowed to retaliate. Meanwhile, Vice-President Vance is headed to Pakistan again for peace talks, but Tehran says it has no plans for further talks with the US.

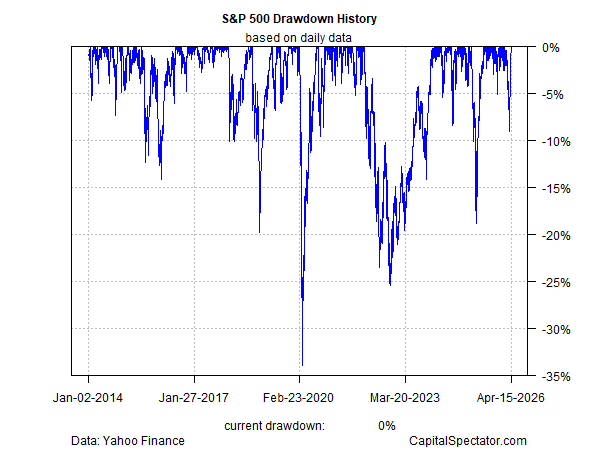

What this means for markets is anyone’s guess, but equities begin the week from a position of strength. The S&P 500 Index’s recovery set a record for speed, but the drama may not be over just yet. The key challenge is that while stocks priced in an effective end to the war, it’s still not obvious that a quick solution the supply-energy shock is imminent.

“We had the most violent day in the strait on Saturday that we’ve had since the beginning of this crisis, and things don’t seem to be getting any better,” Rory Johnston, founder of Commodity Context, tells CNBC. “While we keep getting these sell-offs and it keeps seeming like we’re about to finally get that football — Lucy pulls it away — and we’re back to where we started. The strait still isn’t flowing, and 13 million barrels a day of production remains shut-in. We’re losing it every single day this goes on.”

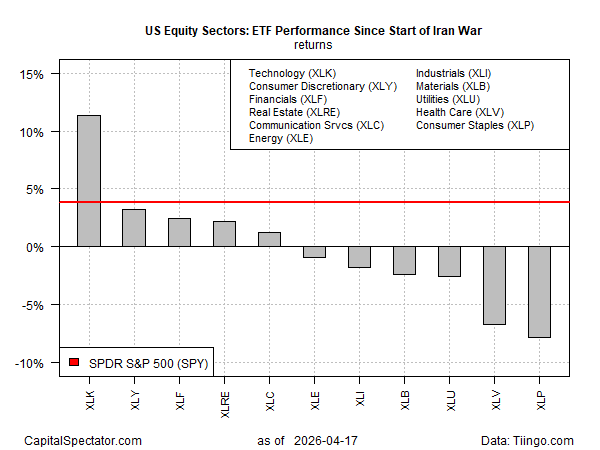

As for the resiliency in the stock market through Friday’s close, much of the hefty lifting comes from technology stocks. Using a set of ETFs to track the sectors that comprise the S&P 500 highlights that tech (XLK) is the leading source of gains by far when measured since the war’s start through the end of last week. XLK is up more than 11% during the conflict, far above the S&P 500’s 3.8% rise since Feb. 28. The rest of the sectors are split with a mix of gains and losses.

Upbeat earnings news is a key factor for the stock market’s overall resiliency. FactSet reports: “For Q1 2026 (with 10% of S&P 500 companies reporting actual results), 88% of S&P 500 companies have reported a positive EPS surprise and 84% of S&P 500 companies have reported a positive revenue surprise.”

In terms of performance, however, tech is still doing the hefty lifting, largely thanks to optimism, overbaked or not, related to the business opportunities in artificial intelligence (AI).

Therein lies a familiar question for investors that’s taken on greater relevance: Can bullish sentiment fueled by AI keep the party going in what could be a protracted battle over reopening the strait?

One reason that the bulls are still answering “yes” relates to expectations of the disinflationary effect of AI for the economy. Citing that “many companies are talking about efficiency gains from AI,” the head of Northern Trust’s $1.4 trillion asset management unit predicts: “If even a portion of those [gains] actually materialize on an economy-wide basis, it could be one of the biggest positive supply shocks we’ve ever seen,” Mike Hunstad tells the FT. “You can’t ignore that.”

By that reasoning, the “massively disinflationary” outlook he thinks is possible leaves room for the Fed to stand pat on monetary policy until it’s clear how AI-driven productivity gains evolve.

“AI has the potential to be massively disinflationary,” Hunstad advises.

Perhaps, but whether that’s enough to keep stocks rallying in the short term is another question entirely.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}