US–Iran Crisis Edges Toward Prolonged Stalemate

President Trump is warning that the US could restart strikes on Iran, a stance that reads less like a negotiating tactic and more like the opening move in a drawn‑out standoff. A few days ago, he described the fragile cease-fire as being on “massive life support.” In other words, a long, grinding stalemate appears to be taking shape. That’s a threat to the global economy because as the impasse drags on and energy exports from the Gulf remain blocked, the world’s oil supply shrinks and scarcity risks rise.

“From the point of view of energy, this is a snowball — and every week that passes, you have tighter markets,” says Jaime Brito, executive director of refining and oil products at Dow Jones Energy.

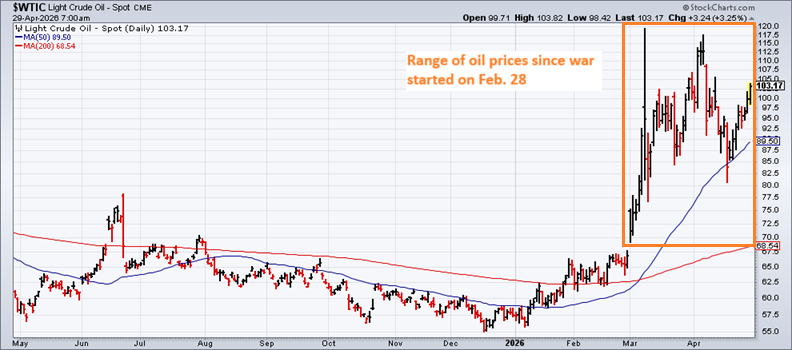

Oil prices reflect that uncertainty. The US benchmark, West Texas Intermediate, traded near $107 a barrel yesterday — a middling range following the surge since the war began.

Brent crude, the global benchmark, is trading closer to its upper range, reflecting the higher level of vulnerability for Europe and Asia related to oil imports relative to America’s domestic oil supplies. A break higher from the current $107 level for Brent would signal that the market is starting to price in a higher risk that the conflict’s stalemate will have deeper and longer‑lasting effects on the global economy, including inflation.

Recent developments behind the scenes aren’t encouraging. A troubling report suggests Iran has tightened its control over the Strait of Hormuz after establishing a new Persian Gulf Strait Authority and positioning itself as the sole gatekeeper for this strategic energy corridor.

According to Lloyd’s List Intelligence, the agency is now demanding that vessels submit application forms for passage — an effort to control transit approvals and collect tolls. Iran’s Islamic Revolutionary Guard Corps (IRGC) “has imposed a de facto ‘toll booth’ regime in the Strait of Hormuz, requiring vessels to submit full documentation, obtain clearance codes and accept IRGC‑escorted passage through a single controlled corridor.”

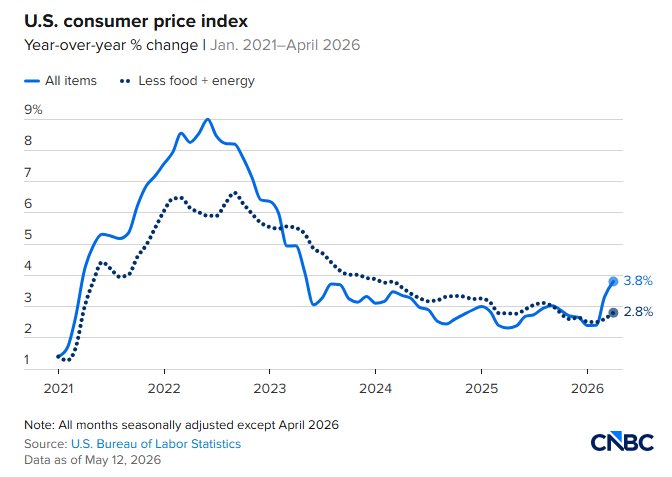

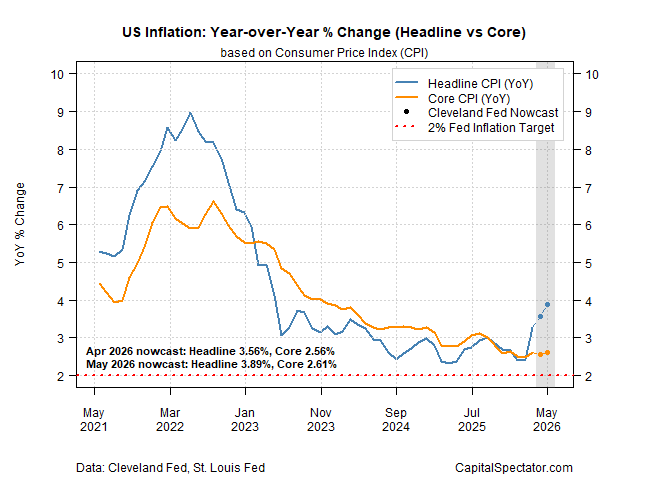

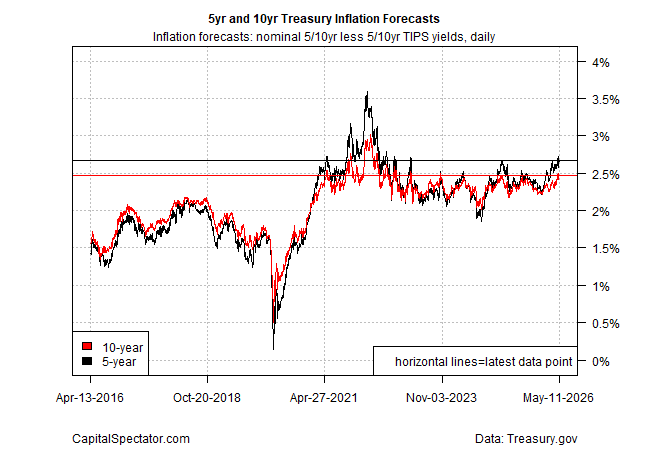

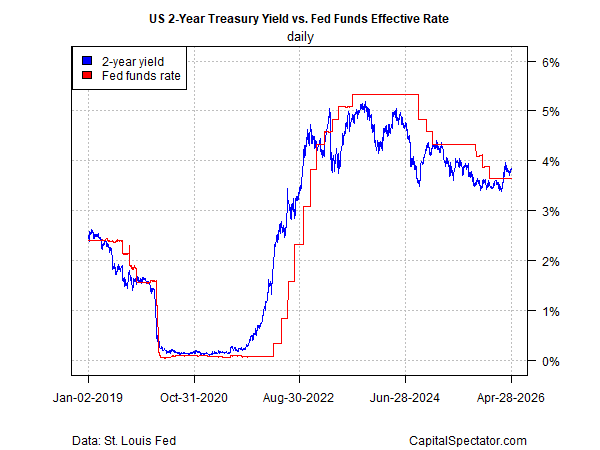

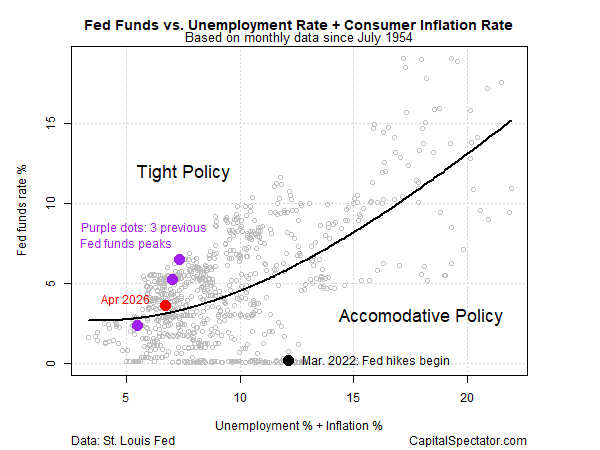

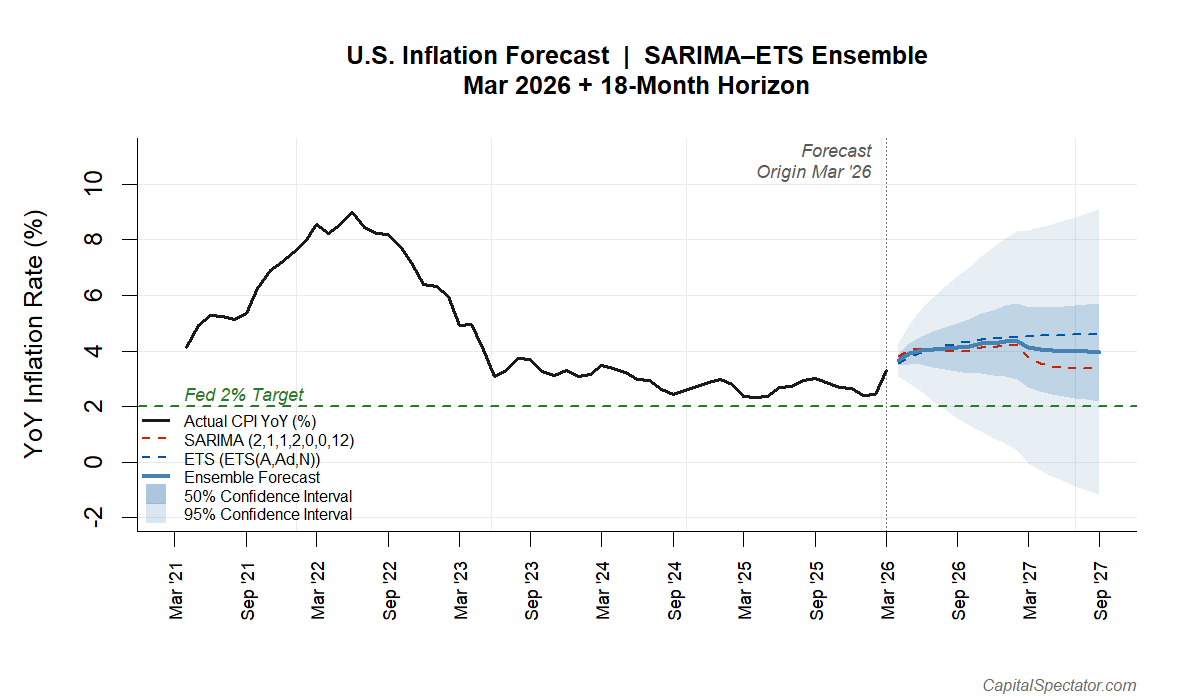

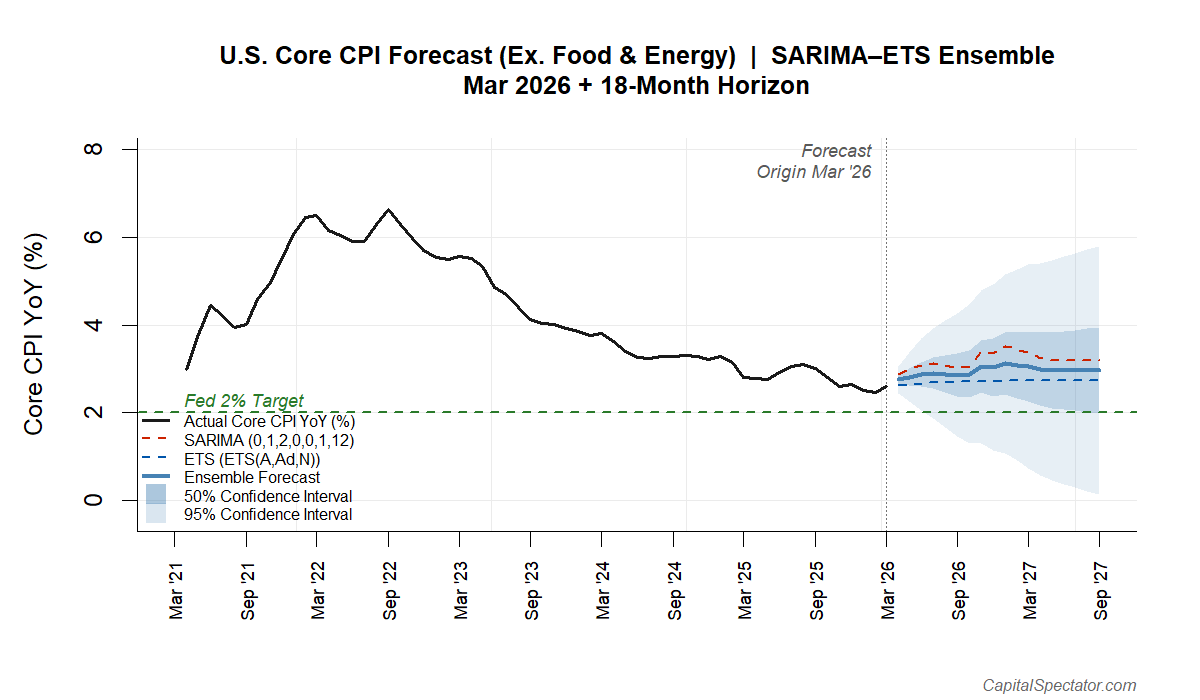

The immediate economic threat is inflation, which continues to rise. Headline consumer inflation increased 3.8% in April from a year earlier — a three‑year high, the Bureau of Labor Statistics reported on Tuesday. The main driver: higher energy costs.

“Inflation is the key drag on the U.S. economy now,” said Heather Long, chief economist at Navy Federal Credit Union. “This is hurting Americans. There is a real financial squeeze underway. For the first time in three years, inflation is eating up all wage gains. This is a setback for middle‑class and lower‑income households, and they know it.”

Inflation will ease once the Middle East crisis is resolved. Unfortunately, the path out of the stalemate isn’t clear, and the US — and the West — increasingly looks boxed in. A resumption of military strikes might break the gridlock, but Iran’s regime has already shown it can take a beating and still maintain its stranglehold over Gulf exports.

Meanwhile, President Trump’s summit with China’s President Xi Jinping may yield a breakthrough, according to some analysts. But before departing Washington for Beijing, Trump downplayed the potential for engaging China to persuade Iran to open the Strait.

“I don’t think we need any help with Iran,” Trump said. “We’ll win it one way or the other, peacefully or otherwise.”

Exactly what that means — and on what timeline — is unclear. In the meantime, the clock is ticking, and the risk of a deeper, longer energy shock continues to rise.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}